Nitrogen Fertilizer Alternatives in Sub Saharan Africa

Introduction

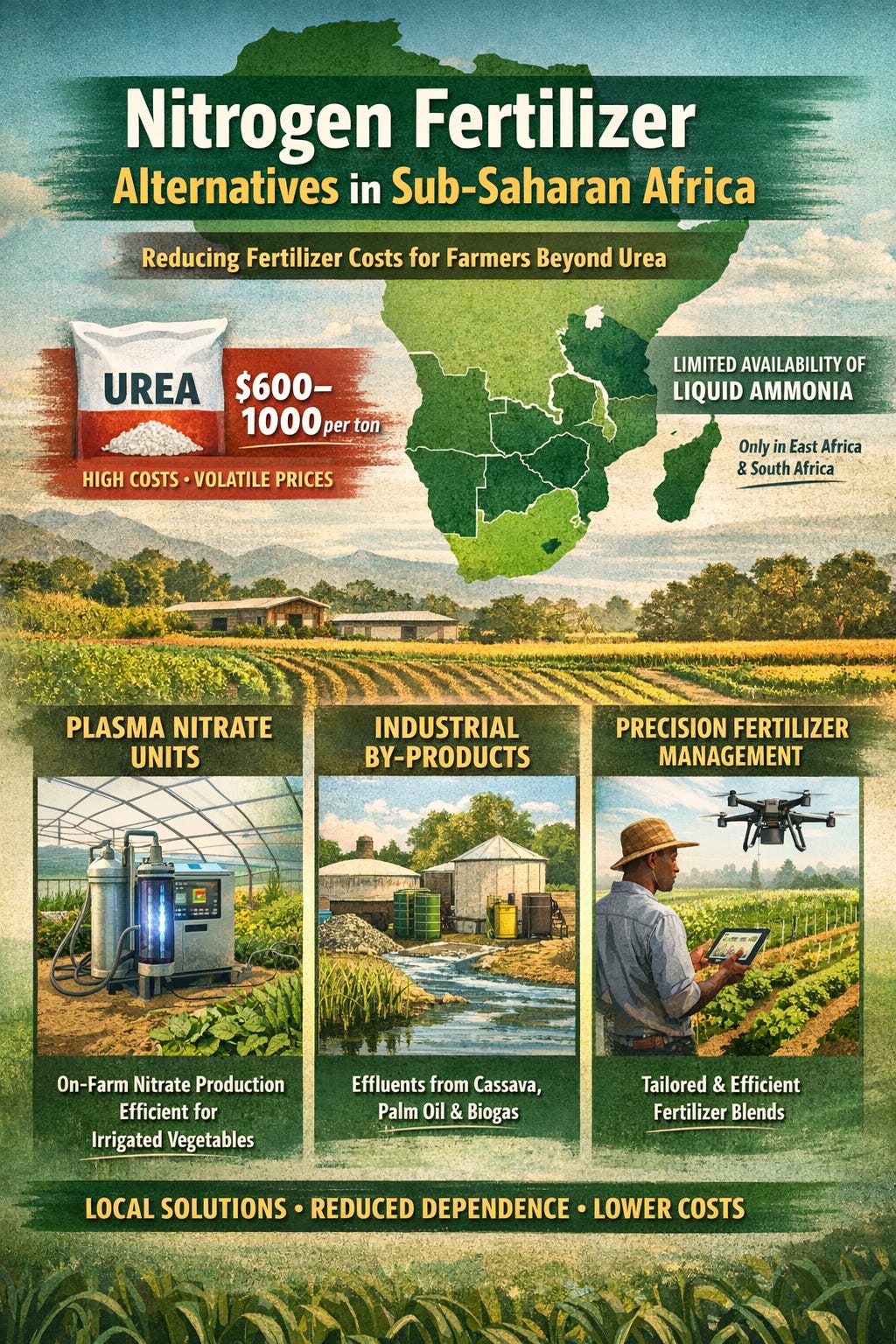

Across Sub‑Saharan Africa (SSA), fertilizer costs have become one of the most pressing challenges for farmers. Urea, the dominant nitrogen source, has swung between $600 and $1000 per metric ton in recent years. For enterprises producing vegetables year‑round, this volatility translates into tens of thousands of dollars in annual costs. The question is clear: are there viable alternatives to urea that can deliver nitrogen predictably, at competitive cost, and in forms crops can use?

This article explores the dependency on urea, the limited availability of ammonia, and the enterprise‑specific alternatives that are emerging across SSA: plasma nitrate units, industrial by‑products, and precision fertilizer management. It draws on real farm economics to show where these alternatives can compete, even when urea prices ease back to $600 per ton.

The Urea Dependency

Urea is the backbone of nitrogen fertilization in SSA. It is 43% nitrogen, easy to transport, and widely available. But it comes with two major drawbacks:

Price volatility: Farmers are exposed to global energy markets and shipping costs. A surge in natural gas prices or shipping disruptions can send urea costs soaring.

Agronomic inefficiency: Urea must hydrolyze before plants can use it, and losses through volatilization can be significant. In hot climates, up to 30% of applied nitrogen can be lost before crops absorb it.

Case Study: 25 ha Vegetable Enterprise

Consider a farmer cultivating 25 hectares of vegetables year‑round, producing about 60 hectares of output annually. Vegetables typically require 250 kg of nitrogen per hectare per year. That’s 15,000 kg of nitrogen annually.

To meet this demand with urea (43% N), the farm needs 35 metric tons annually.

At $1000/ton, that’s $35,000 per year.

Even at $600/ton, the cost is still $21,000 per year.

This dependency on imported urea is unsustainable for many enterprises. It exposes farmers to global price swings and erodes profitability.

Liquid Ammonia: Limited Availability

Globally, ammonia is a predictable nitrogen source. It can be applied directly or converted into urea and ammonium nitrate. But in SSA, liquid ammonia is only available in four East African countries (Kenya, Tanzania, Ethiopia, Uganda) and South Africa. For most of West Africa, including Liberia, ammonia is not accessible.

This means that for the majority of SSA farmers, ammonia is not a practical alternative. Unless new production or import infrastructure is built, urea remains the default nitrogen source. The search for alternatives must therefore focus on technologies and resources that can be deployed locally.

Plasma Nitrogen Units

One of the most promising innovations is plasma nitrate technology, sometimes called “green lightning.” These units use electricity to split air molecules, producing nitrate and nitrite directly in water.

Cost: A unit costs about $6000 upfront, amortized over five years at ≈ $1200/year, plus electricity and water purification.

Agronomy: Nitrate is immediately plant‑available, efficient in fertigation, and reduces volatilization losses compared to urea.

Enterprise fit: Irrigated vegetable farms and cooperatives. Weekly fertigation cycles align perfectly with plasma nitrate output.

Competitiveness: Against $21,000–35,000 annual urea costs, plasma nitrate can be competitive if efficiency gains reduce nitrogen demand by 20–30%.

For vegetable enterprises, plasma nitrate offers a serious alternative. It delivers nitrogen in the form crops prefer, reduces losses, and fits into irrigation systems. The challenge is ensuring reliable electricity and clean water — conditions not always met in rural SSA. But where infrastructure exists, plasma nitrate can rival urea on both cost and agronomic performance.

Industrial By‑products

Agro‑processing industries generate nutrient‑rich residues such as biogas digestate and effluents. These by‑products contain measurable nitrogen, though content varies and requires testing.

Cost: Often free or low‑cost; transport is the main expense.

Agronomy: Nitrogen content is variable but measurable; requires standardization to ensure predictable application.

Enterprise fit: Farms near agro‑industry hubs (cassava, sugar, palm oil, breweries).

Competitiveness: Can partially substitute urea demand, reducing costs and import dependency.

Industrial by‑products are not a universal solution, but they can be powerful in specific contexts. In agro‑industry clusters, farmers can tap into waste streams that provide nitrogen at minimal cost. With proper testing and blending, these by‑products can reduce reliance on imported urea.

Precision Fertilizer Management (SSNM / Blended Fertilizers)

Site‑Specific Nutrient Management (SSNM) uses soil testing and tailored blends to optimize nitrogen use. It doesn’t replace fertilizer, but it ensures that every kilogram applied is used efficiently.

Cost: Requires investment in soil testing and advisory services.

Savings: At $600/ton urea, SSNM can cut bills by 15–30% (saving $3,000–6,000 annually in the 25 ha case).

Agronomy: Predictable, ensures consistent yields while lowering input costs.

Enterprise fit: Larger farms with access to soil data and extension services.

SSNM is less about finding new nitrogen sources and more about using existing ones better. For enterprises with the capacity to collect data, SSNM can deliver significant savings and improve yields.

Regional Perspectives

East Africa: Farmers in Kenya, Tanzania, Ethiopia, and Uganda have access to liquid ammonia, but infrastructure limits its use to larger enterprises. Plasma nitrate pilots are emerging in horticulture.

West Africa: Urea dominates, with limited alternatives. Industrial by‑products from cassava and palm oil processing offer opportunities, but plasma nitrate units could be transformative for vegetable enterprises.

Southern Africa: South Africa has ammonia infrastructure and more advanced SSNM adoption. Larger farms are experimenting with blended fertilizers and precision application.

Outlook for SSA Farmers

The landscape of nitrogen fertilizers in SSA is shaped by availability, infrastructure, and enterprise type.

Vegetable enterprises: Plasma nitrate units are the most promising alternative, offering predictable nitrogen at competitive cost.

Agro‑industry clusters: Industrial by‑products can substitute part of urea demand, reducing costs and import dependency.

Large farms: SSNM and blended fertilizers stretch every kilogram of nitrogen further.

Liquid ammonia: Only relevant in East and Southern Africa; not an option for most SSA farmers.

For most of SSA, urea remains the default nitrogen fertilizer. But its high cost and inefficiency make alternatives increasingly attractive. Plasma nitrate, industrial by‑products, and SSNM represent fair, enterprise‑specific solutions that are both economically competitive and agronomically predictable. These options allow farmers to reduce dependency on volatile imports and build more resilient fertilizer strategies.

Conclusion

Nitrogen is the lifeblood of modern agriculture, but in SSA it comes at a steep price. Urea at $600–1000 per ton forces farmers into difficult choices. Liquid ammonia is only available in limited regions. The real alternatives are enterprise‑specific: plasma nitrate for irrigated vegetables, industrial by‑products for farms near agro‑industry hubs, and SSNM for larger enterprises.

These solutions are not ideological; they are practical. They offer farmers predictable nitrogen at competitive cost, tailored to their enterprise type. By adopting them, SSA farmers can reduce dependency on volatile imports, improve efficiency, and build resilience in the face of global market shocks.